Nordic Electricity Market – Q1 2026

During Q1 2026, the Nordic electricity market continued to experience volatility in imbalance prices, with higher price levels and less negative prices. Market participants are showing signs of adapting their behavior to the 15-minute markets.

This report reviews key developments in the Nordic electricity markets during the first quarter of 2026 from an imbalance settlement perspective. It focuses on imbalance prices, volumes, and market participant behavior as the market continues to adapt to 15-minute trading. The report is based on data available at the time the imbalance settlement for the quarter is closed.

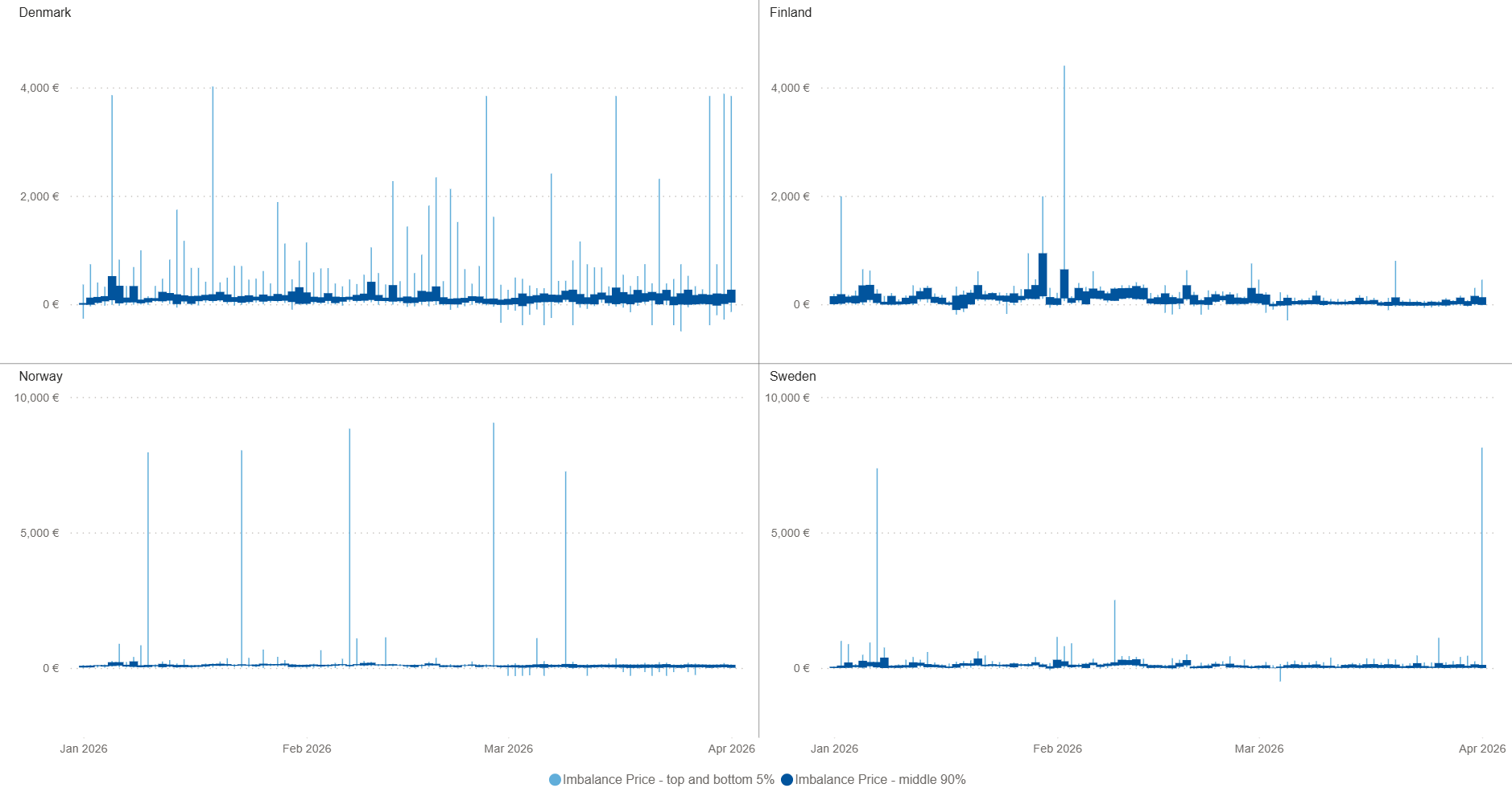

Imbalance prices remain volatile with fewer negative prices

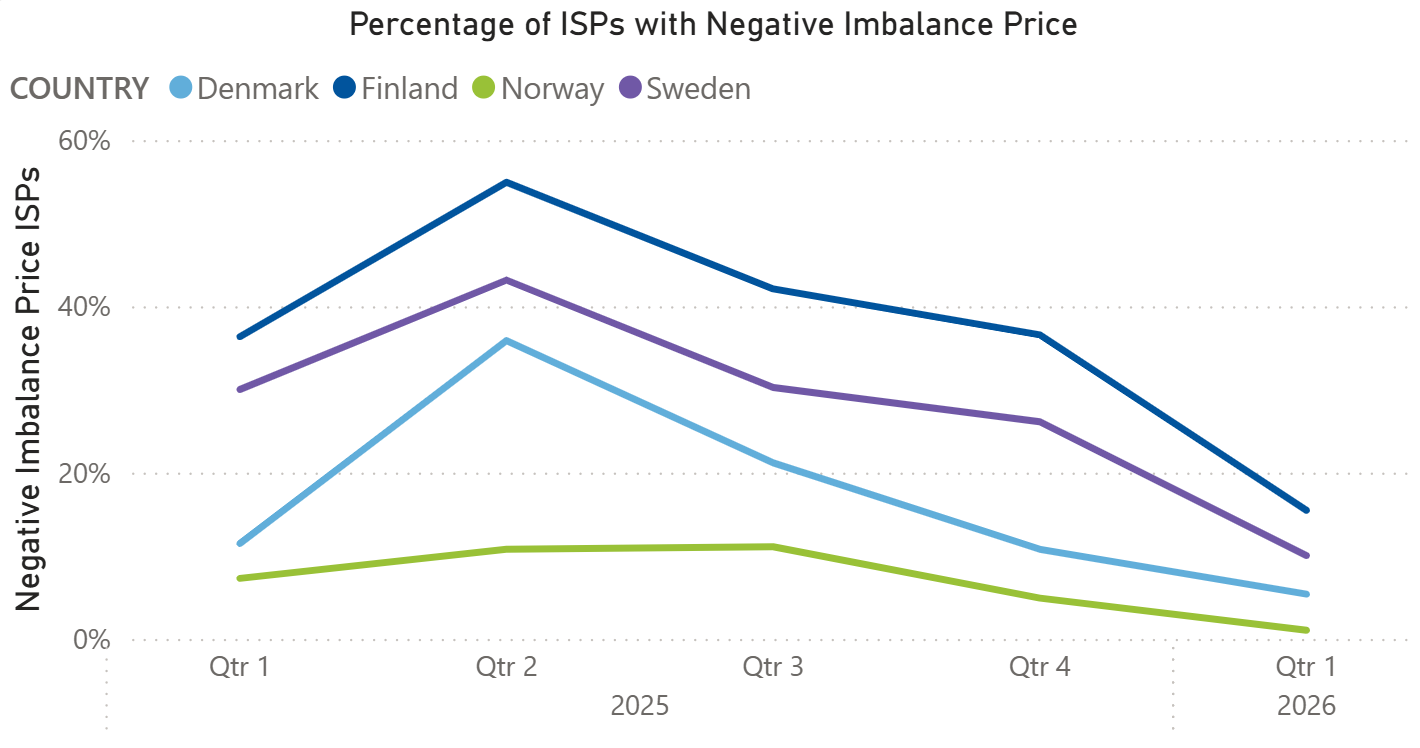

Imbalance prices remained volatile during Q1 2026, with price spikes occurring at regular intervals across all Nordic countries. The volatility has persisted since the introduction of the mFRR EAM in March 2025. In addition, the high electricity price levels in January and February were reflected in imbalance prices, contributing to a generally higher imbalance price level during the quarter. Negative imbalance prices were less frequent during the quarter compared to earlier periods.

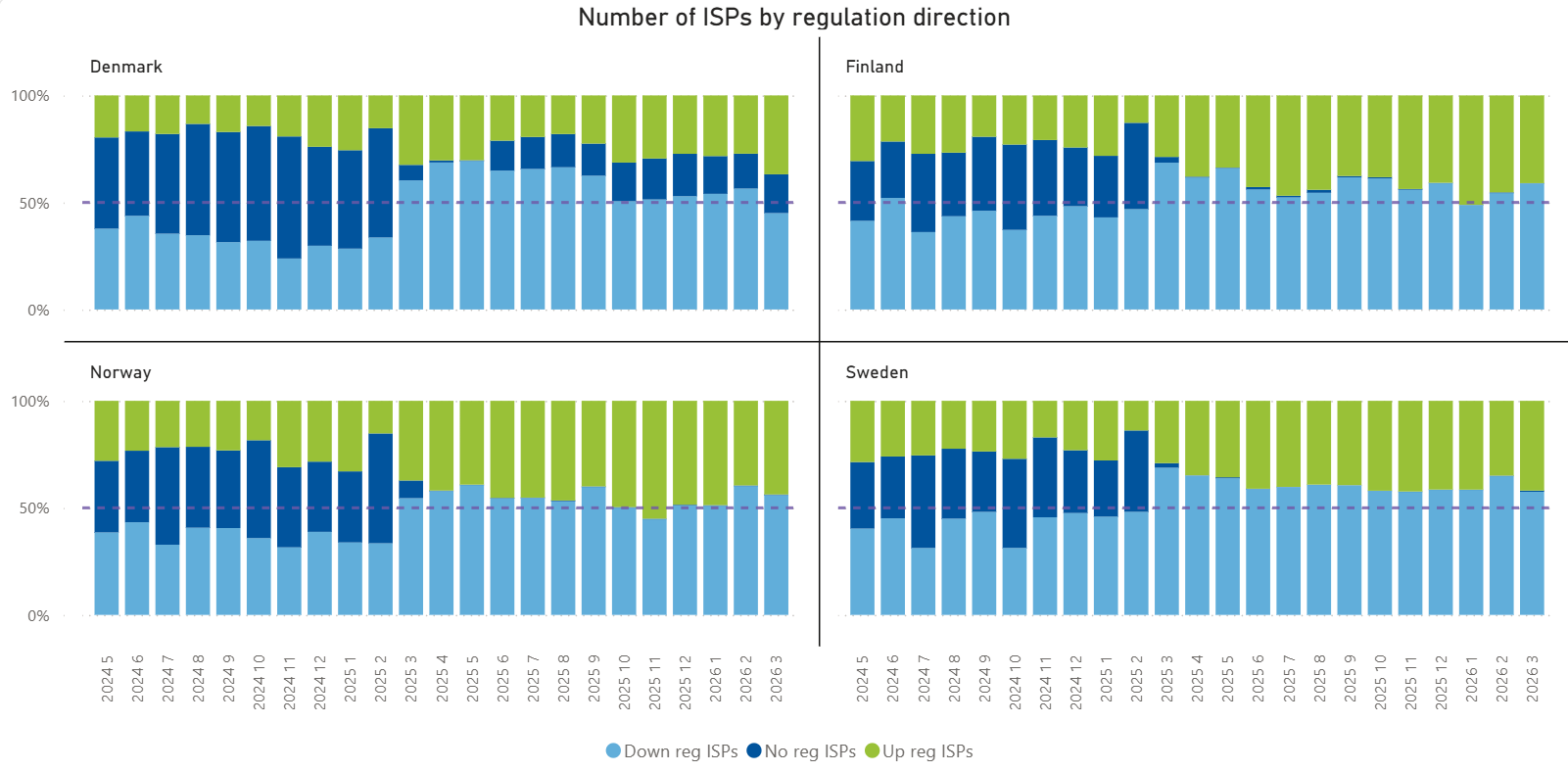

ISPs with no regulation direction continue to be nonexistent except for Denmark, where a deadband on scheduled mFRR activations was implemented in June 2025. In general, in all countries down-regulation ISPs are more common than up-regulation ISPs. Among the countries, Norway shows the most even balance between up- and down-regulation.

Imbalance volumes remain broadly stable, while trends differ between countries

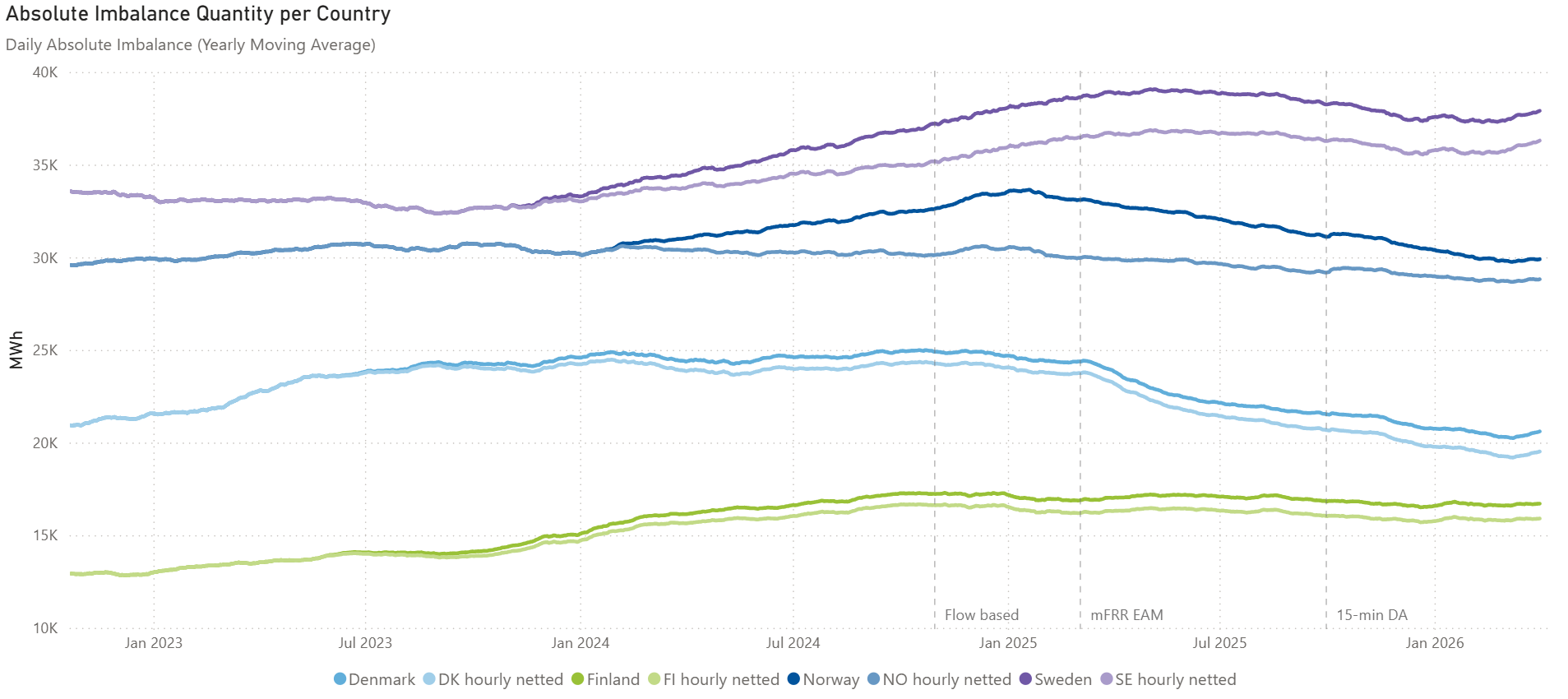

Absolute imbalance quantities remained broadly stable during the first quarter across the Nordic region, although trends differ between countries. Denmark stands out with a clear decrease in imbalance volumes following the introduction of the mFRR Energy Activation Market (EAM) in March 2025. This development is likely linked to the more volatile imbalance prices since the introduction of the mFRR EAM, strengthening incentives for Balance Responsible Parties to actively minimize imbalances. In contrast, imbalance volumes in Finland and Sweden remained broadly stable, with levels in Q1 slightly higher than in the previous quarter. Norway continues to show a longer-term declining trend.

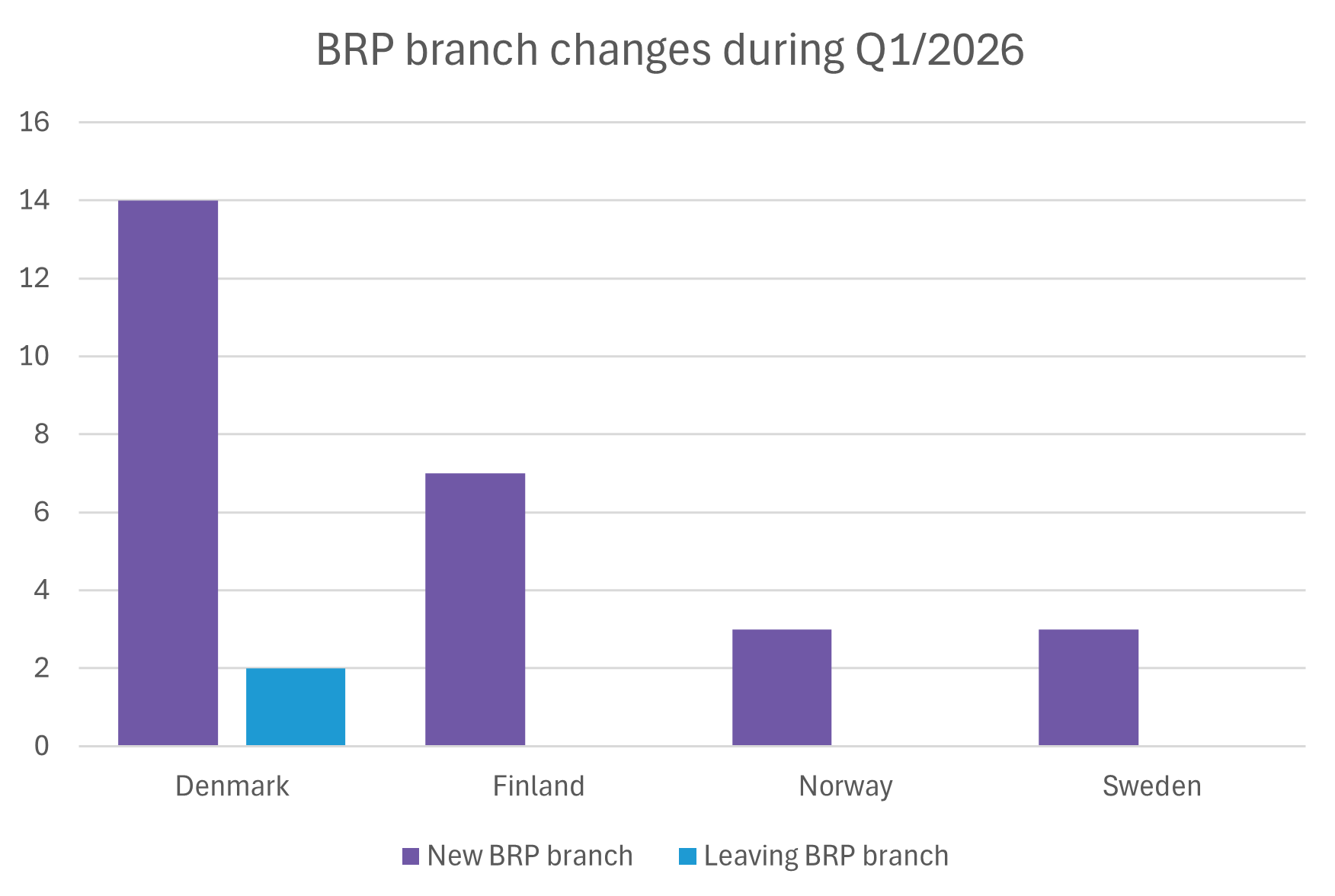

Trader BRPs continues to account for most new market entries

The number of BRPs continued to grow in Q1 2026. The figure shows new and leaving BRP branches registered during the quarter by country, with a total of 27 new BRP branches. Most new BRPs entering the market are traders, who continue to account for the majority of the growth.

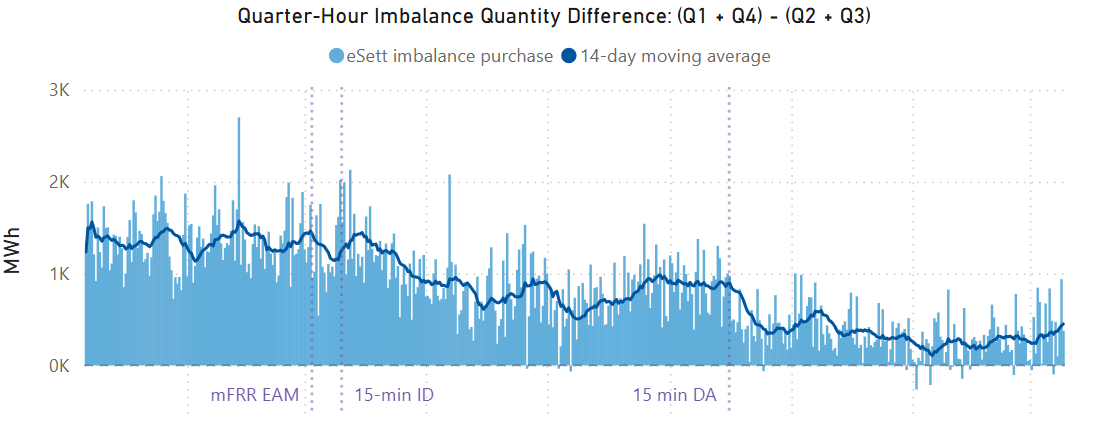

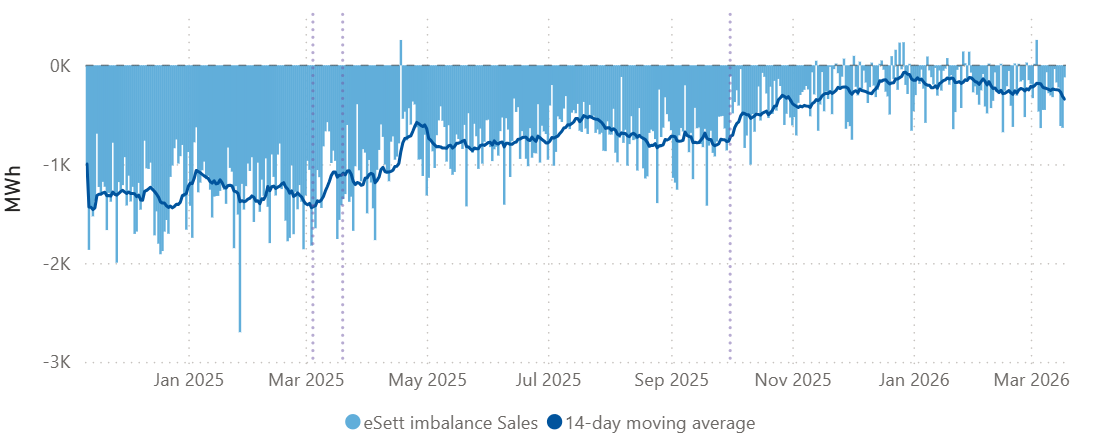

Market participants are adapting to 15‑minute markets

After the move to 15‑minute imbalance settlement in May 2023, imbalances were initially higher in the first and last quarters of the hour (Q1 and Q4). This reflected a transitional phase where many market parties still structured their positions on an hourly basis, with volumes placed in the first or last 15‑minute interval. The figure highlights how quarter‑hour imbalance patterns have evolved during the transition to 15‑minute trading. Last year, as 15‑minute trading was introduced first in intraday and later in the day‑ahead market, this pattern faded. The more even distribution of imbalances across all quarter hours shows that market parties have increasingly adapted to the 15‑minute framework and are managing their positions more consistently throughout the hour.

Looking Ahead

The Nordic electricity market has undergone significant changes in recent years. Now the market enters a period where no major changes in market design are expected in the near term, allowing the focus to shift from change to practice. This provides market participants with time to learn, adapt, and further optimize their operations to the new market environment.